Bill Gates is often quoted as having said that “Most people overestimate what they can achieve in a year and underestimate what they can achieve in ten years” so to complement our 20th anniversary celebrations were using that principle but doubling Bill’s timeline.

Every month during 2023 we’re going to take an important global data point from the year we were founded, 2003, compare it with the same data point now and see what lessons we can draw from that.

And we’re starting with the big one: CO2 emissions.

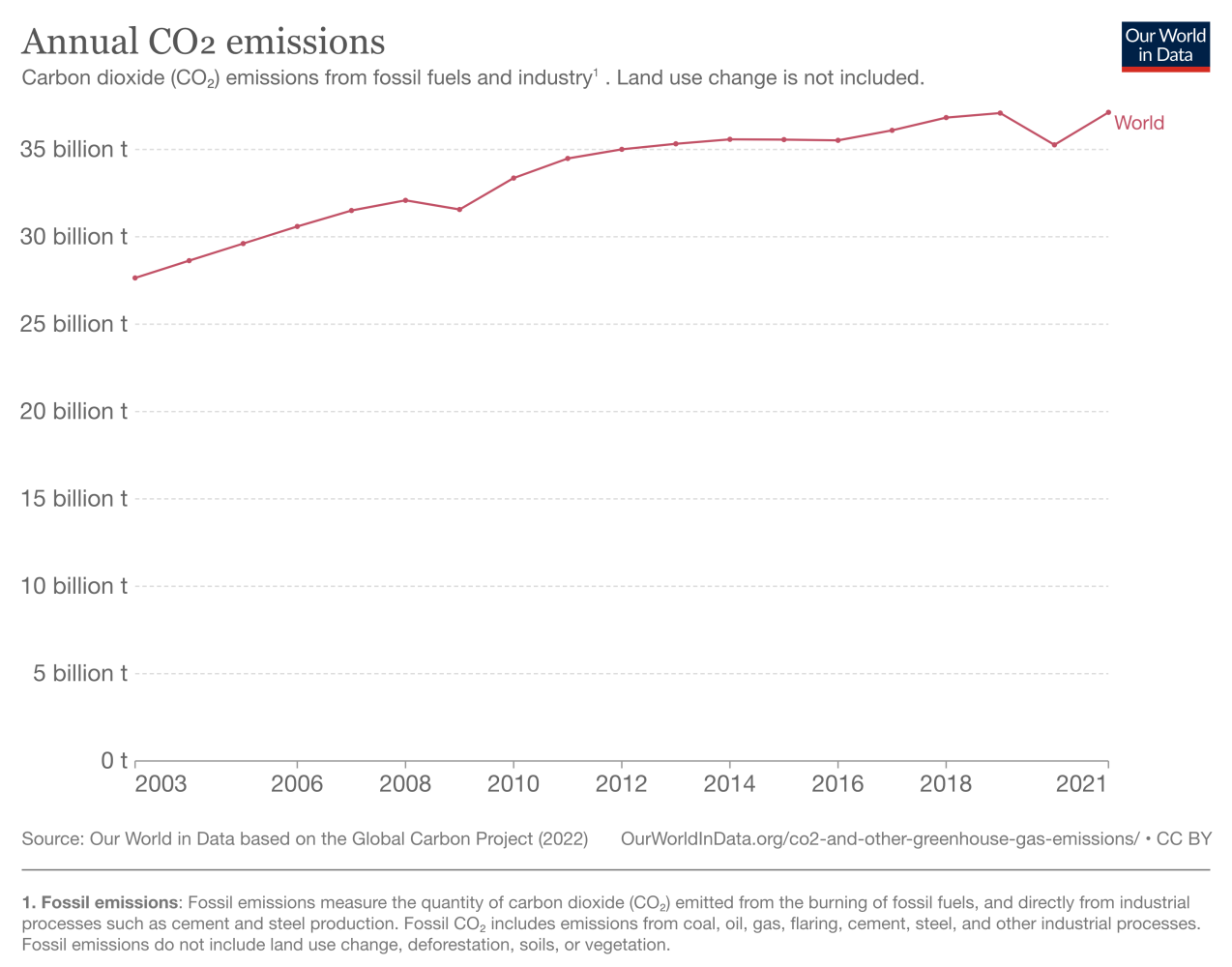

Whilst our banner graphic above shows the downward trend for UK emissions over the last 20 years, thanks to the brilliant team at Our World in Data you can see below the truth of the situation globally – and it isn’t pretty.

We can see clearly what happened when we were all in various states of lockdown – in truth not that much – and might even convince ourselves that, to coin a phrase, we’re flattening the curve.

But when you consider that as relatively recently as 1950 annual emissions were just 6 billion tonnes per year compared with 35+ billon now, the impact of the way we live is staring us (in fact very often either blowing a gale, wave or flame) directly in the face.

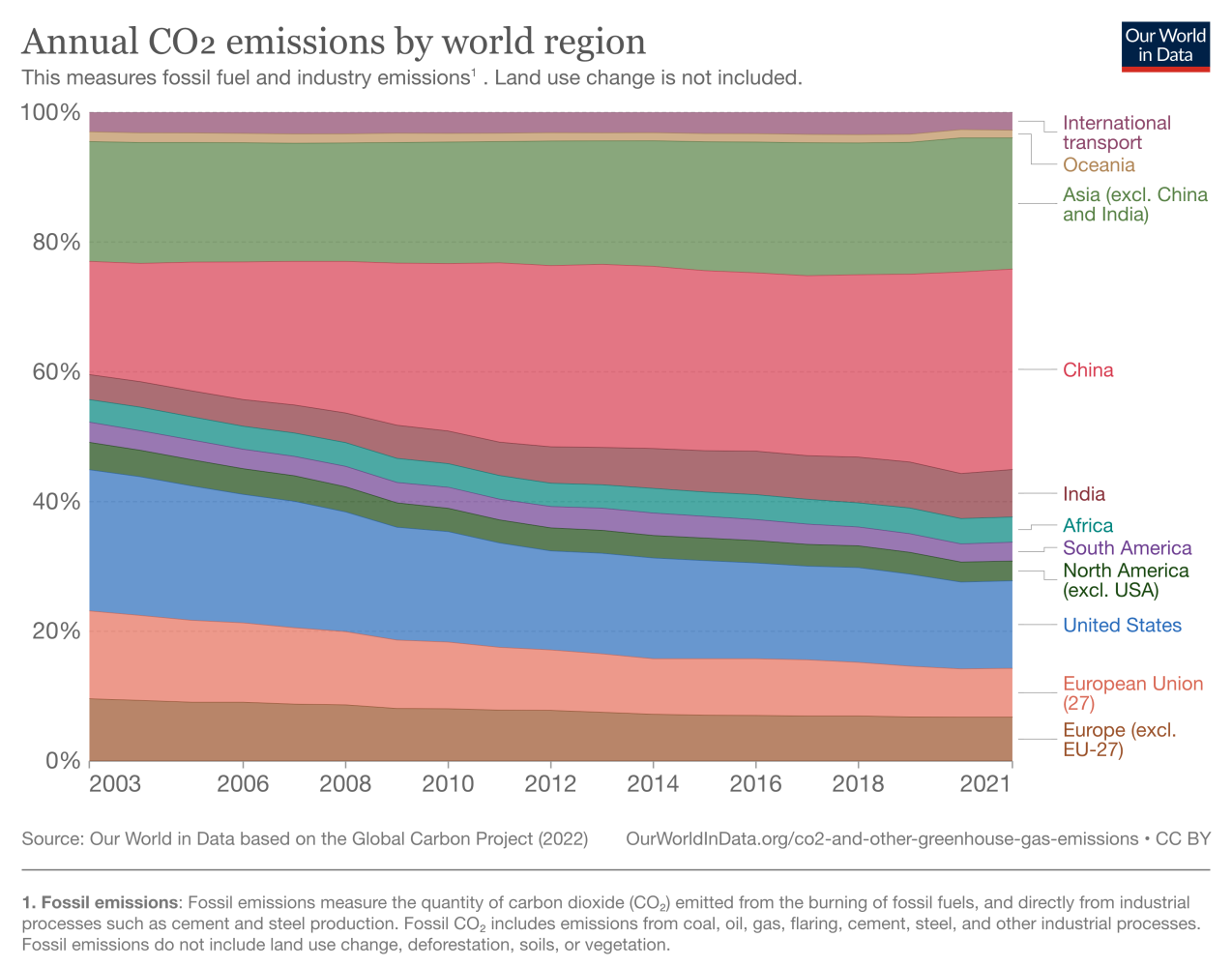

So, which regions are emitting the most and are any of us moving fast enough to limit the worst affects of climate change?

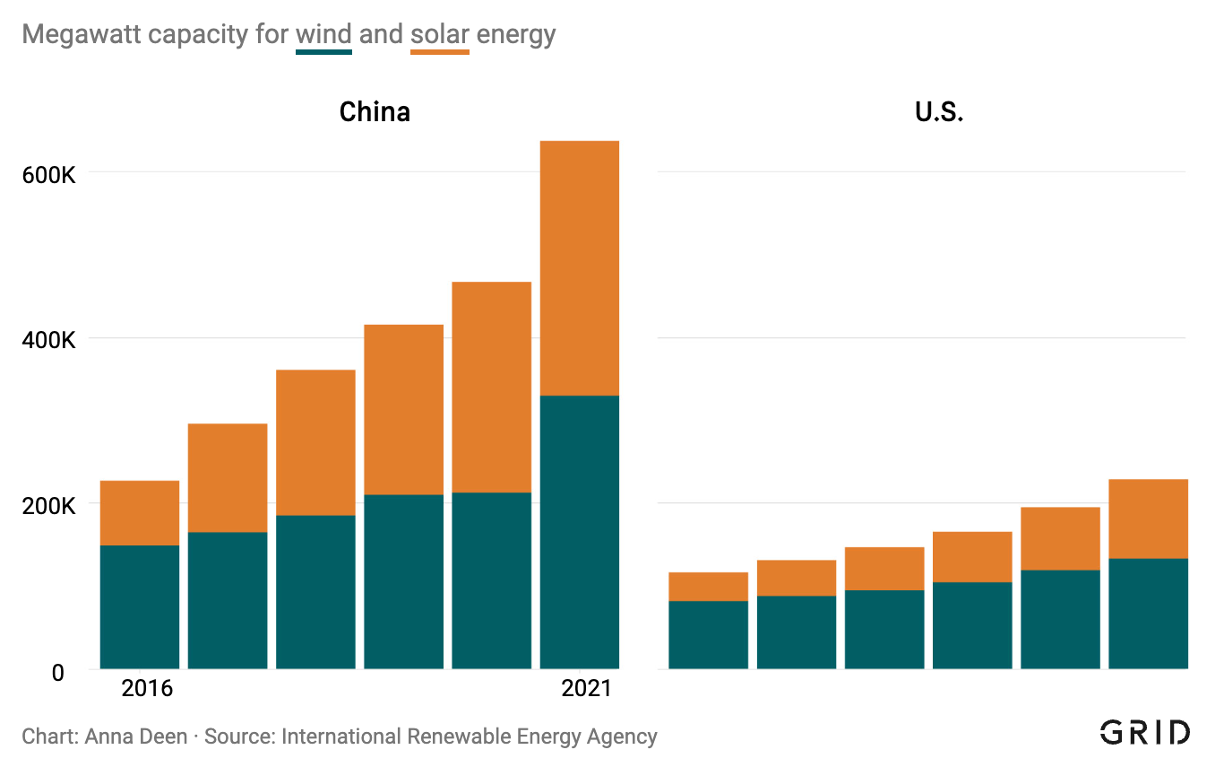

Yes, over our 20 year window the EU and the US have reduced their emissions whereas China has grown but that masks the massive historical emissions that Western countries put into the atmosphere in the second half of the 20th century.

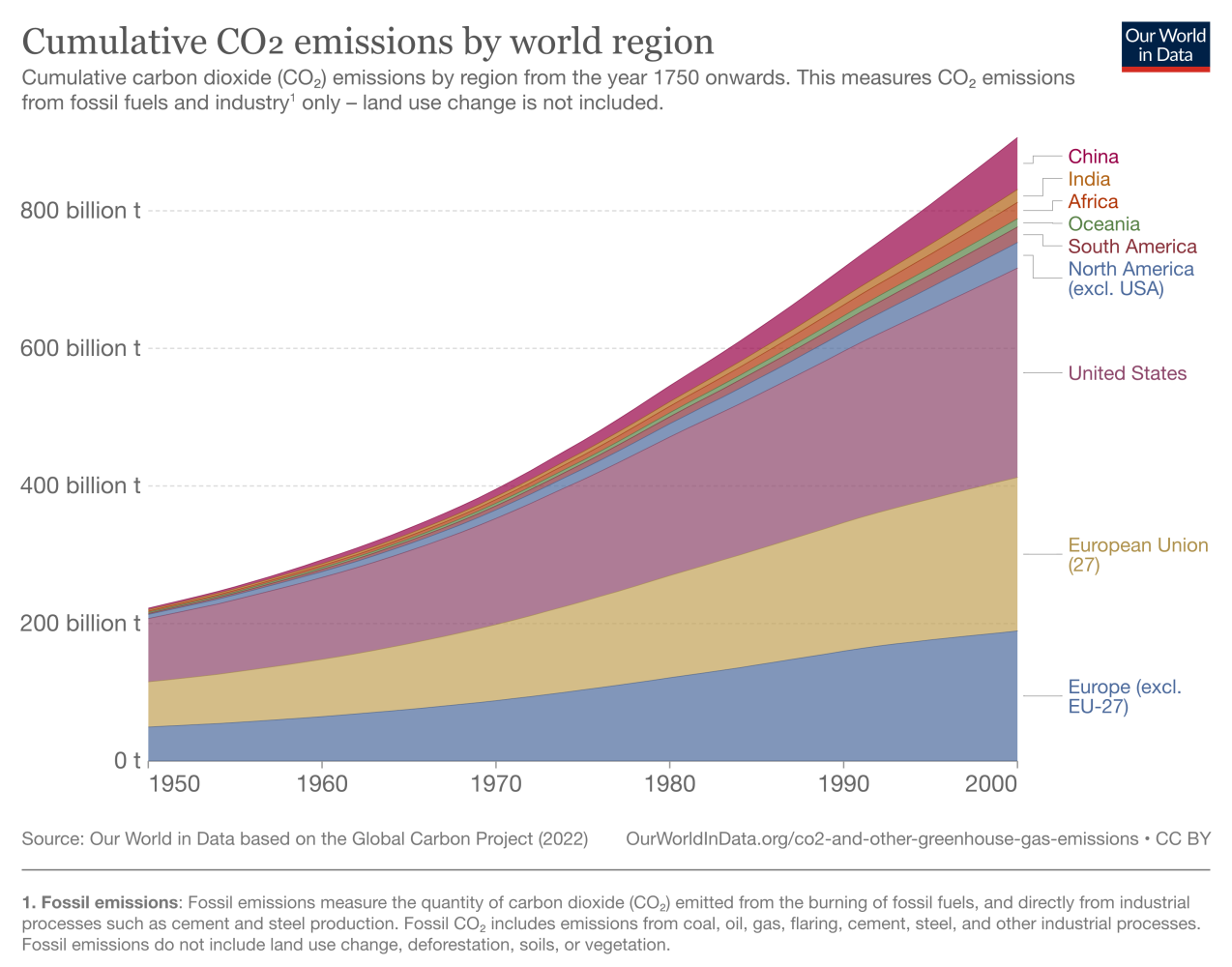

Allow us a moment to shift from a 20 to a 50 year view.

It’s pretty much statistically impossible that China – and certainly not India, Africa or South America – will ever emit anything like the cumulate emissions of the US and the EU not least because they are in fact also the leading builders of renewable energy production.

Yes, China is still building new coal fired power plants and that’s got to stop quickly but making this a geopolitical contest about who is the most virtuous now achieves nothing, especially since our global climate has no interest in borders.

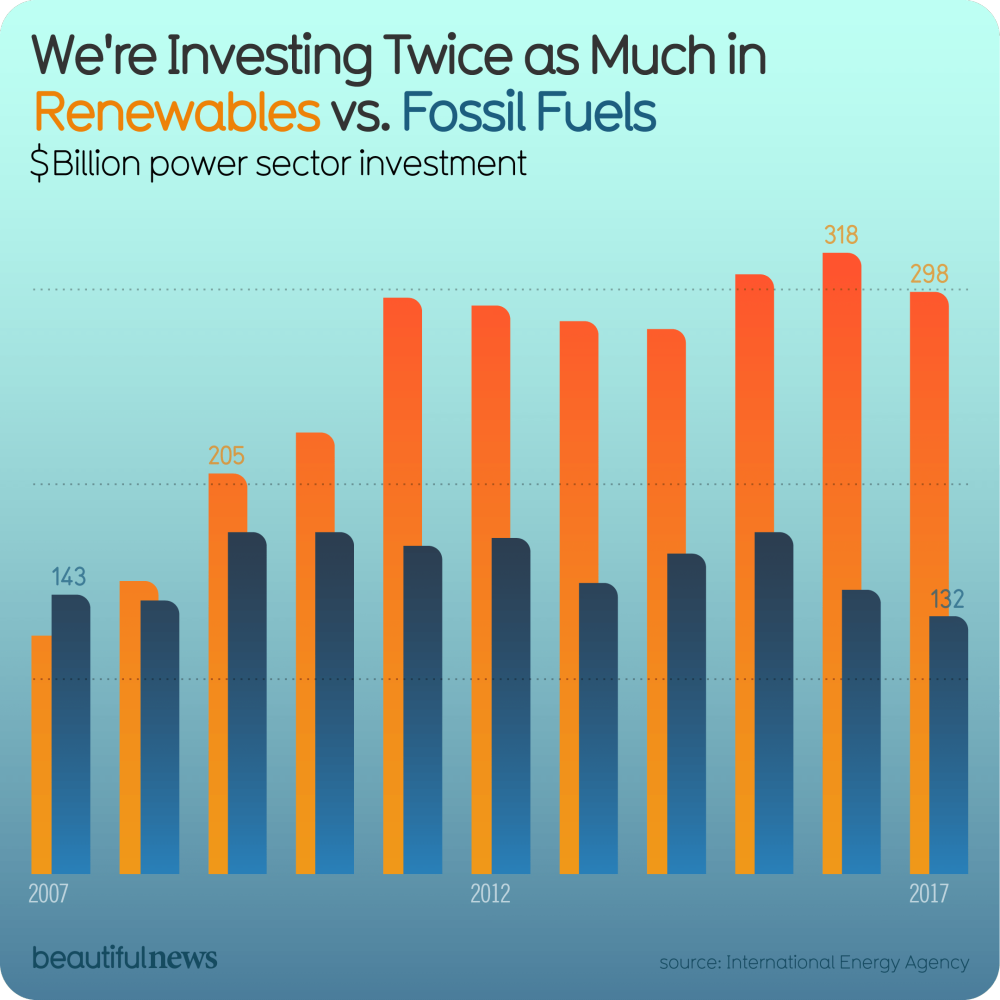

Every country has finally woken up to this and we’re now in a race to see how quickly the exponential effect of renewable investment and technology advancement can compete with the undeniable and accelerating affects of years of inaction.

So, whilst macro infrastructure build is happening what can businesses like yours and ours do to better play our part?

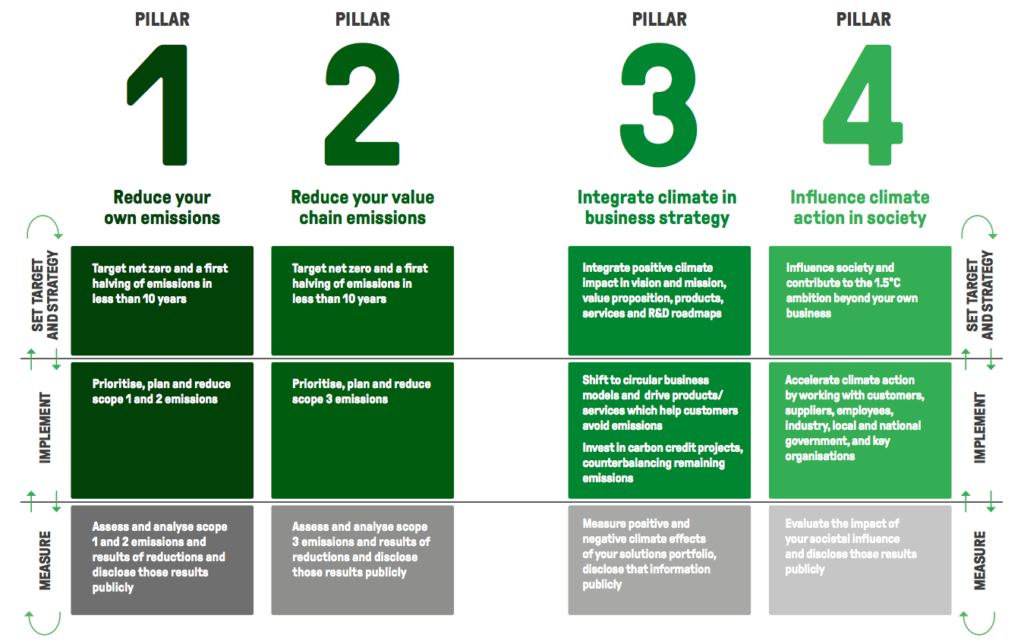

Back in 2020 the World Economic Forum produced a very helpful 1.5°C Business Playbook that proposes four pillars for any business large or small:

Most of our clients are well on the way with pillars 1 and 2 but there isn’t a moment for complacency in either of them. Pillar 3 is appearing a little more often, especially with consumer focused organisations, but in truth has much further to go and pillar 4 is where we all, us at Positive Momentum, a Certified B Corp®very much included, have really got to push harder.

In our Earth First diagnostic we challenge clients to consider whether they are Compliant (meeting the regulations for their industry), Sustainable (hitting net zero across all activities) or Regenerative (doing things that remove carbon from the atmosphere and therefore paying back their historical ‘carbon debt’). More than diagnosing, this tool offers a clear and practical path from one level to the next.

Our pledge as a proud B Corp UK is to become Regenerative to the extent that we pay back all of our carbon emissions from the last 20 years within the next 3 years. It’s a bold and ambitious objective but we’ve done the maths and established the processes to make it a reality.

We’re acutely aware in writing this piece that everyone we know is doing something and many are doing a lot but our challenge to everyone is to ask every day what more you can do?

How ever much any of us are doing, we know by looking at the current trajectory of the graphs that it isn’t enough.

Technology is coming and coming fast but we’ve collectively left that investment until the last possible minute – and we have to face the fact that emissions have not yet peaked.

A widespread rapid change in consumer behaviour clearly isn’t coming to our rescue.

In any event – and whether you like it or not – our economies cannot withstand the scale of change it would take to get the trend of emissions into reverse immediately.

But, we’re optimists at Positive Momentum, a Certified B Corp® and we totally believe that businesses will be the force that leads the history books to look back on this period and reflect on how when it really mattered the collective ingenuity and drive of the commercial world was the difference that made the difference. We see it every day in our work and we’re looking forward to the day (much sooner than January 2043) when the data proves Bills assertions but that this became the greatest underestimation of progress the world has ever known.